guidelines established by the PRISMA 2020 statement (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) to ensure methodological rigor, transparency, and reproducibility in the research process (Page et al., 2021).

METHODOLOGY

Study Design

This study was developed as a systematic review, a secondary research methodology that enables the rigorous identification, evaluation, and synthesis of the available scientific evidence on a specific topic (Kitchenham & Charters, 2007). This approach was selected because it provides a structured framework that minimizes the biases inherent in traditional narrative reviews, ensuring greater objectivity and reproducibility in the research process.

The review was conducted and reported according to the PRISMA 2020 statement (Preferred Reporting Items for Systematic Reviews and Meta-Analyses), which is the most widely recognized and adopted methodological standard for systematic reviews in the international scientific community (Page et al., 2021). Adherence to this protocol ensures transparency, facilitates critical appraisal by other researchers, and allows for eventual replication of the study.

Formulation of the Research Question

Before initiating the systematic search, the research question was formulated using the PICO format adapted for exploratory scoping reviews:

a) Population: Entrepreneurial ventures, entrepreneurs, microenterprises, and small businesses in Peru

b) Intervention/Exposure: Use of digital wallets (Yape, Plin, Tunki, BIM, among others)

c) Comparison: Not applicable for this review

d) Outcomes: Evidence on the impact, adoption, benefits, or challenges of using digital wallets in the entrepreneurial context

This structure made it possible to precisely delimit the scope of the review and guide the construction of the search strategy in a manner consistent with the stated objective.

Search Strategy: Construction of the Search Equation

A Boolean search equation was designed and structured into three thematic blocks connected by the AND operator, ensuring that retrieved results contained terms related to each of the three essential components: digital wallets, entrepreneurship, and the Peruvian context.

Within each thematic block, the OR operator was used to connect synonyms, linguistic variants, and specific denominations, thereby maximizing the sensitivity of the search. The inclusion of terms in both Spanish and English responded to the need to capture literature published in both languages, considering that journals indexed in international databases frequently publish in English, whereas local scientific production tends to be disseminated in Spanish.

The final search equation was structured as follows:

("billetera digital" OR "billeteras digitales" OR "billetera móvil" OR "billeteras móviles" OR "billetera electrónica" OR "billeteras electrónicas" OR "digital wallet" OR "digital wallets" OR "mobile wallet" OR "mobile wallets" OR "e-wallet" OR "e-wallets" OR "mobile payment" OR "mobile payments" OR "pago móvil" OR "pagos móviles" OR "pago digital" OR "pagos digitales" OR "Yape" OR "Plin" OR "Tunki" OR "BIM" OR "fintech") AND ("emprendimiento" OR "emprendimientos" OR "emprendedor" OR "emprendedores" OR "entrepreneur" OR "entrepreneurship" OR "MYPE" OR "MYPES" OR "PYME" OR "PYMES" OR "microempresa" OR "microempresas" OR "pequeña empresa" OR "pequeñas empresas" OR "negocio" OR "negocios" OR "startup" OR "startups" OR "comercio" OR "comerciante" OR "vendedor" OR "vendedores" OR "bodega" OR "bodegas") AND ("Perú" OR "Peru" OR "peruano" OR "peruanos" OR "peruana" OR "peruanas" OR "peruvian")

The decision to include the names of specific Peruvian digital wallets (Yape, Plin, Tunki, and BIM) was based on the need to capture studies that might refer to these platforms without necessarily using the generic term "digital wallet." Likewise, the inclusion of terms such as "bodega" and "merchant" reflects the particularities of the Peruvian entrepreneurial context, where these actors represent a significant proportion of the business fabric.

Selection of Databases

The systematic search was conducted on March 17, 2025, in four databases strategically selected to ensure comprehensive coverage of the available scientific literature:

a) Scopus: This database was included because it is one of the largest sources of peer-reviewed literature worldwide, covering multiple disciplines, including the social sciences, economics, and management. Its coverage of Latin American journals has increased significantly in recent years, making it relevant to the study context.

b) Web of Science Core Collection: This database was selected because of its recognized prestige and rigorous criteria for indexing scientific journals. Although it has historically had less representation of Latin American literature than other databases, its inclusion ensures the capture of studies published in high-impact international journals.

c) SciELO (Scientific Electronic Library Online): The incorporation of this database was essential because it is the main open-access platform for Latin American scientific literature. Its regional focus allows the retrieval of studies developed in contexts similar to Peru and published in Ibero-American journals that may not be indexed in international databases.

d) DOAJ (Directory of Open Access Journals): This database was included because it specializes in open-access journals worldwide, complementing the search in the other databases and enabling the identification of literature that may not be indexed in Scopus or Web of Science but meets editorial quality standards.

Decision Not to Apply Filters

No filters for publication date, language, or document type were deliberately applied during the search. This methodological decision was based on several arguments:

First, the digital-wallet phenomenon in Peru is relatively recent, having experienced its greatest expansion after 2016 with the launch of BIM and later with Yape (2017) and Plin (2020). Therefore, applying a time restriction could have led to the exclusion of pioneering studies documenting early adoption experiences.

Second, the literature on this specific topic in the Peruvian context is still emerging and presumably limited. Applying restrictive filters could have significantly reduced the number of retrieved studies and compromised the comprehensiveness of the review.

Finally, not applying filters made it possible to obtain a complete overview of the state of knowledge on the topic, identifying not only scientific articles but also other types of academic documents that could provide relevant evidence.

Independent Search Process

To minimize human error and ensure the reliability of the search process, the search was carried out independently by each of the two authors of the study. Each researcher executed the search equation in the four selected databases, recorded the number of results obtained, and downloaded the corresponding records.

Subsequently, both authors compared the results obtained independently, confirming complete agreement in the findings identified in each database. This double-verification procedure, recommended by methodological guidelines for systematic reviews (Higgins et al., 2019), increases the reliability of the process and reduces the probability of omitting relevant studies due to errors in search execution.

Search Results

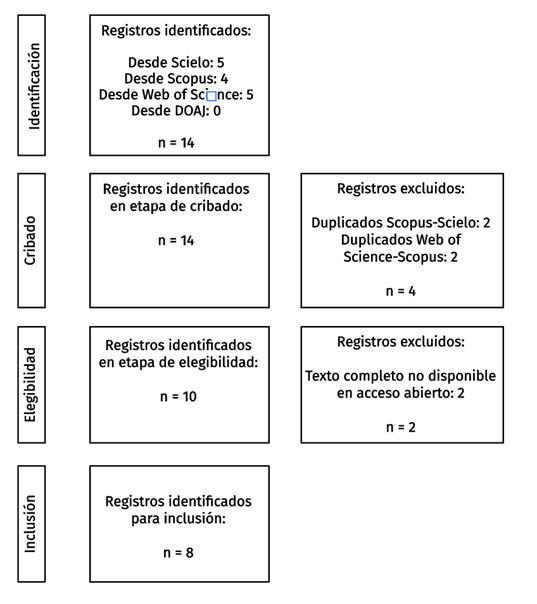

The search strategy yielded a total of 14 records distributed across the four databases consulted. Table 1 presents the results obtained from each information source in detail:

Table 1 | Search results by database

|

Database |

Records Identified |

Duplicates |

Not Accessible |

Studies Included |

|

SciELO |

4 |

0 |

0 |

4 |

|

Scopus |

5 |

2 |

1 |

2 |

|

Web of Science Core Collection |

5 |

2 |

1 |

2 |

|

DOAJ |

0 |

0 |

0 |

0 |

|

Total |

14 |

4 |

2 |

8 |

Note. The search was conducted on March 17, 2025. Duplicates correspond to studies indexed simultaneously in multiple databases.

The results show that SciELO was the most productive source in terms of unique studies included, which was expected given its focus on Latin American literature. Scopus and Web of Science contributed similar numbers of records, although with considerable overlap between the two, reflecting the multiple indexing typical of journals with greater international visibility.

The absence of results in DOAJ, despite its broad coverage of open-access journals, suggests that the specific literature on digital wallets and entrepreneurship in Peru is concentrated in journals indexed in the other consulted databases, or that the terms used in the search equation did not match the terminology used in publications indexed in DOAJ.

Of the 14 records initially identified, 4 corresponded to duplicates present in multiple databases, specifically studies indexed simultaneously in SciELO and Scopus or in Scopus and Web of Science. These duplicates were identified and removed by comparing titles, authors, and DOI when available.

In addition, 2 studies identified in Scopus and Web of Science, respectively, could not be incorporated into the review because they were available only through subscription or payment models, with no full-text access through the researchers' institutional subscriptions or open-access repositories. Although this limitation reduces the final number of included studies, it reflects the real restrictions faced by researchers in contexts with limited access to scientific journal subscriptions.

After removing duplicates and inaccessible records, 8 studies were selected for inclusion in the systematic review.

Eligibility Criteria

The definition of clear inclusion and exclusion criteria is a fundamental element in systematic reviews, as it objectively delimits which studies will be considered for the synthesis and which will be excluded (Higgins et al., 2019). The criteria established for this review were as follows:

Inclusion Criteria

Studies were included when they met all of the following criteria:

a) Thematic relevance: Studies that explicitly addressed the relationship between digital wallets and entrepreneurship, whether by analyzing the impact of these technologies on ventures, adoption patterns among entrepreneurs, perceived benefits, challenges faced, or any other dimension linking both phenomena.

b) Geographic context: Research that included specific evidence on the Peruvian context. Studies conducted exclusively in Peru, as well as comparative or regional studies that included data or analysis referring to the Peruvian case, were considered.

c) Type of publication: Scientific articles published in indexed journals, prioritizing those subjected to peer-review processes that ensure a minimum standard of methodological quality.

d) Availability: Studies with full-text access, either through open access, institutional repositories, or subscriptions available to the researchers.

e) Methodological design: Empirical studies with quantitative, qualitative, or mixed approaches, as well as theoretical or conceptual studies providing analytical frameworks relevant to understanding the phenomenon studied.

f) Language: Publications in Spanish or English, considering that these are the predominant languages in the scientific literature on the topic and the languages in which the researchers were competent to conduct the analysis.

Exclusion Criteria

Studies were excluded when they presented any of the following characteristics:

a) Absence of Peruvian evidence: Studies that, despite addressing digital wallets and entrepreneurship, did not include specific data, analysis, or references to the Peruvian context. Studies on other Latin American countries were excluded unless they explicitly incorporated comparisons with the Peruvian case.

b) Non-scientific publications: Opinion articles, editorials, letters to the editor, journalistic notes, or documents without rigorous empirical or theoretical support. Although such documents may provide valuable perspectives, their inclusion would compromise the methodological homogeneity of the review.

c) Duplicates: Records identified in multiple databases, retaining only one version to avoid overrepresentation of particular studies in the synthesis.

d) Inaccessibility: Studies whose full text could not be obtained through any available mechanism, including open access, repositories, institutional subscriptions, or contact with authors.

e) Exclusively technical focus: Studies centered solely on technological, cybersecurity, or systems-architecture aspects of digital wallets, with no link to business or entrepreneurial dimensions.

Selection Process

The study-selection process was developed according to the four phases established in the PRISMA 2020 protocol, each with specific objectives and clearly defined procedures:

Phase 1: Identification

In this initial phase, the search equation was executed in each of the four selected databases. The retrieved records were exported in formats compatible with reference-management software to facilitate subsequent processing. The exact number of results obtained in each database, as well as the search execution date, was recorded, which is essential for ensuring process reproducibility.

Phase 2: Screening

During the screening phase, duplicate records were identified and removed. This process was initially carried out automatically using reference-management software, followed by manual verification to identify duplicates not detected automatically due to variations in the transcription of titles or authors' names. The unique records resulting from this process advanced to the next evaluation phase.

Phase 3: Eligibility

In this phase, each non-duplicate record was assessed against the previously established inclusion and exclusion criteria. The assessment was conducted in two stages: first by reading titles and abstracts to discard clearly irrelevant studies, and then by reading the full text for those that passed the first filter. Studies whose full text could not be accessed were excluded at this stage, and the reasons for exclusion were documented in each case.

Phase 4: Inclusion

The final phase consisted of defining the definitive set of studies to be submitted to the qualitative synthesis. The 8 studies that met all inclusion criteria and passed the previous phases were incorporated into the review, after which systematic data extraction was conducted.

PRISMA Flow Diagram

The study-selection process is graphically represented in Figure 1, following the standardized format proposed by the PRISMA 2020 statement. This diagram transparently displays the flow of records through the different phases of the review, as well as the reasons for exclusion at each stage.

Figure 1 | PRISMA flow diagram of the study identification, screening, eligibility, and inclusion process

Data Extraction

A standardized matrix was designed for the systematic extraction of information from the included studies, enabling the uniform collection of relevant data from each investigation. The variables included in the extraction matrix were defined according to the review objective and the expected characteristics of studies on the topic:

a) Bibliographic data: Authors, year of publication, study title, journal name, volume, issue and pages, as well as the DOI when available.

b) Study objective: Main purpose stated by the authors, allowing the specific focus of each study to be understood.

c) Methodological design: Type of research (descriptive, correlational, explanatory, exploratory), methodological approach (quantitative, qualitative, mixed), data-collection techniques used, and characteristics of the study sample or participants.

d) Digital wallet studied: Identification of the specific platforms analyzed in each study (Yape, Plin, Tunki, BIM, or others), or whether the study addressed digital wallets generically.

e) Type of entrepreneurship analyzed: Characterization of the ventures studied according to size (microenterprise, small business), economic sector, degree of formalization, geographic location, or other relevant variables.

f) Main findings: Synthesis of the most relevant results reported by the authors in relation to the objective of this review.

g) Reported limitations: Methodological or scope-related restrictions acknowledged by the authors of each study.

Data extraction was carried out independently by both authors for the first three studies, and the results were subsequently compared to verify consistency in interpretation and information recording. Once agreement on extraction criteria was reached, the remaining studies were distributed between the authors for individual processing.

Methodological Quality Assessment

The methodological quality of the included studies was assessed using scientific-rigor criteria adapted to the design of each study. Given that the identified studies presented diverse methodological designs (quantitative, qualitative, and mixed), a single standardized assessment tool was not used; instead, general quality criteria applicable across designs were considered:

a) Clarity and coherence in the formulation of objectives or research questions

b) Adequacy of the methodological design in relation to the stated objective

c) Sufficient description of data-collection procedures

d) Validity and reliability of the instruments used (in quantitative studies)

e) Credibility and transferability of the findings (in qualitative studies)

f) Coherence between the results presented and the conclusions formulated

g) Recognition of study limitations

It is important to note that, following methodological recommendations for systematic reviews in the social sciences (Petticrew & Roberts, 2006), the quality assessment was not used as an exclusion criterion, but rather as an element to contextualize the findings and weigh the strength of the reported evidence.

Synthesis of Information

Considering the heterogeneity identified in the methodological designs, theoretical approaches, and variables analyzed in the included studies, a narrative synthesis of the findings was conducted instead of a quantitative meta-analysis. This approach was appropriate because the diversity of the studies prevented statistical pooling of results while still allowing patterns, convergences, and divergences in the available evidence to be identified (Popay et al., 2006).

To facilitate systematic understanding and comparison of the included studies, the extracted information was presented through structured tables that organized the data in a standardized manner. This presentation strategy made it possible to visualize clearly and orderly the characteristics of each study, facilitating both comparative analysis and the identification of trends in the reviewed literature.

The synthesis tables included the following dimensions of analysis:

a) Bibliographic data: Authors, year of publication, study title, journal name, volume, issue and pages, as well as the DOI when available. This information enabled precise identification of each study and facilitated its location by readers interested in consulting the primary sources.

b) Study objective: Main purpose stated by the authors, enabling the specific focus of each investigation and its particular contribution to the field of knowledge on digital wallets and entrepreneurship in Peru to be understood.

c) Methodological design: Type of research (descriptive, correlational, explanatory, exploratory), methodological approach (quantitative, qualitative, mixed), data-collection techniques used, and characteristics of the study sample or participants. This information was essential for assessing the methodological strength of each study and appropriately contextualizing its findings.

d) Digital wallet studied: Identification of the specific platforms analyzed in each study (Yape, Plin, Tunki, BIM, or others), or whether the study addressed digital wallets generically. This datum made it possible to map which platforms received greater research attention and which remained underexplored in the literature.

e) Type of entrepreneurship analyzed: Characterization of the ventures studied according to size (microenterprise, small enterprise), economic sector, degree of formalization, geographic location, or other relevant variables. This dimension was crucial for understanding the scope of the findings and their applicability to different segments of the Peruvian entrepreneurial ecosystem.

f) Main findings: Synthesis of the most relevant results reported by the authors in relation to the objective of this review. This column constituted the core of the synthesis, condensing the evidence that directly answered the research question.

g) Reported limitations: Methodological or scope-related restrictions acknowledged by the authors of each study. The inclusion of this information enabled a critical reading of the findings and guided the identification of knowledge gaps that future research could address.

This tabular organization allowed not only an orderly presentation of the information but also the identification of cross-cutting patterns, gaps in the literature, and areas requiring further research development in the field of entrepreneurship associated with digital wallets in the Peruvian context.

RESULTS

This section presents the findings derived from the eight studies included in the systematic review. To facilitate comparative reading, the information was organized into four tables: the first summarizes the bibliographic and methodological characteristics of the studies; the second synthesizes the main findings related to digital wallets and entrepreneurship; the third groups the evidence into common thematic axes; and the fourth identifies the limitations reported by each study. This organization made it possible to visualize more clearly both the available evidence and the gaps in the literature.

Table 2 | Search results by database (citation, title, source, objective, and methodological design)

|

No. |

Citation |

Title |

Source |

Study objective |

Methodological design |

|

1 |

Vilcanqui Velazquez et al. (2022) |

Lessons from Remarkable FinTech Companies for the Financial Inclusion in Peru |

Journal of Risk and Financial Management |

To analyze outstanding FinTech companies in other countries in order to extract lessons applicable to financial inclusion in Peru. |

Exploratory-descriptive study with a mixed approach, qualitative benchmarking, and correlational analysis. |

|

2 |

Vera-Acevedo & Iparraguirre-Piedra (2025) |

The influence of consumer trust on the drivers of electronic wallet transactions |

Intangible Capital |

To analyze the relationship between consumer trust and electronic-wallet transactions in Peru. |

Quantitative study, online survey, and PLS-SEM structural modeling. |

|

3 |

Juarez-Alvarez et al. (2025) |

Adoption of digital wallets and their impact on the sales of Peruvian micro-entrepreneurs |

Polish Journal of Management Studies |

To determine the level of acceptance of digital wallets and their impact on the sales of microentrepreneurs in Arequipa. |

Quantitative study, survey, TAM model, correlational analysis, and multiple linear regression. |

|

4 |

Gomez et al. (2022) |

Crowdlending as a financing alternative for MSMEs in Peru |

Retos. Revista de Ciencias de la Administracion y Economia |

To determine whether MSMEs in Piura are willing to demand financing through crowdlending. |

Quantitative, descriptive, cross-sectional study using a survey. |

|

5 |

Vargas Garcia (2021) |

Digital Banking: Technological Innovation in Financial Inclusion in Peru |

Industrial Data |

To determine the relationship between digital banking and financial inclusion in Peru from 2010 to 2019. |

Quantitative, correlational study using Pearson analysis. |

|

6 |

Salazar-Rebaza et al. (2024) |

Use of e-Wallets and Their Impact on SME Business Transactions |

Proceedings of the 19th European Conference on Innovation and Entrepreneurship |

To determine the impact of using electronic wallets on SME business transactions. |

Applied, quasi-experimental, cross-sectional, quantitative study. |

|

7 |

Guardamino & Tostes (2021) |

Qualitative analysis of technology management for financial-service innovation: A multiple case study of FinTech startups in Metropolitan Lima |

New Trends in Qualitative Research |

To analyze technology-management processes for financial-service innovation in FinTech startups in Metropolitan Lima. |

Qualitative multiple-case study, in-depth interviews, and WebQDA analysis. |

|

8 |

Mendoza Rejas et al. (2023) |

Mobile wallets as an alternative payment method for retailers during the pandemic |

Investigacion Negocios & Revista Cientifica |

To determine the impact of the inclusion of mobile wallets as a payment method from the perspective of retail entrepreneurs in Ica. |

Quantitative, exploratory, descriptive, cross-sectional study. |

Table 2 made it possible to identify the main bibliographic and methodological characteristics of the studies included in the systematic review. First, a recent temporal concentration of publications was observed, ranging from 2021 to 2025, which shows that the analysis of digital-wallet use and its relationship with entrepreneurship in Peru is still an emerging field of research. Likewise, the predominance of quantitative studies stood out, as six of the eight works used surveys, correlational analyses, or statistical models to examine the phenomenon. This suggests a tendency in the literature to measure perceptions, levels of acceptance, or relationships between variables, rather than to deepen complex contextual explanations.

Only one study used a qualitative approach and one employed a mixed design, revealing a lower presence of research aimed at understanding in depth the organizational, technological, or social processes associated with the adoption of these tools. Regarding objectives, some studies directly addressed digital wallets and their impact on microentrepreneurs or small businesses, whereas others offered contextual evidence on financial inclusion, digital banking, or the FinTech ecosystem. Overall, the table showed a heterogeneous body of literature that is still consolidating but is sufficiently relevant to support analysis of the phenomenon in the Peruvian context.

Table 3 | Search results by database (citation, context or sample, digital wallet or technology studied, and type of entrepreneurship or unit of analysis)

|

No. |

Citation |

Context / sample |

Digital wallet or technology studied |

Type of entrepreneurship or unit of analysis |

|

1 |

Vilcanqui Velazquez et al. (2022) |

Comparative study of Peru, Kenya, Brazil, the Philippines, and Pakistan. |

BIM and mobile wallets in the Peruvian context; FinTech in general. |

MSMEs, microenterprises, and small Peruvian businesses as indirect beneficiaries. |

|

2 |

Vera-Acevedo & Iparraguirre-Piedra (2025) |

386 users aged 18 to 40 from Metropolitan Lima who had used e-wallets in the previous three months. |

Yape, Tunki, Agora Pay, and Plin. |

Electronic-wallet users; indirect evidence for businesses accepting these payments. |

|

3 |

Juarez-Alvarez et al. (2025) |

120 microentrepreneurs from a shopping center in Arequipa. |

Digital wallets in general; the article mainly mentions Yape and Plin as Peruvian references. |

Microentrepreneurs in the commercial sector. |

|

4 |

Gomez et al. (2022) |

382 MSMEs in the Piura region. |

Crowdlending and the FinTech ecosystem, not digital payment wallets. |

MSMEs in commerce, restaurants, technical services, and other sectors. |

|

5 |

Vargas Garcia (2021) |

Aggregated national data for Peru for the period 2010-2019. |

Digital banking and digital payments. |

Peruvian financial system; indirect evidence for entrepreneurship. |

|

6 |

Salazar-Rebaza et al. (2024) |

88 SMEs in Otuzco, La Libertad; 23 in the control group and 65 in the experimental group. |

Electronic wallets in general. |

SMEs in commerce and services. |

|

7 |

Guardamino & Tostes (2021) |

Four FinTech startups in Lima: Apurata, Difondy, TasaTop, and Tranzfer.me. |

Digital financial innovation; not focused on payment wallets. |

Peruvian FinTech startups. |

|

8 |

Mendoza Rejas et al. (2023) |

385 entrepreneurs from formal retail businesses in the province of Ica. |

Plin, Yape, Tunki, Lukita, and mobile wallets in general. |

Formal retail businesses. |

Table 3 allowed a more precise observation of the empirical contexts in which the included studies were developed, as well as the type of financial technology addressed and the unit of analysis used in each case. First, most studies were concentrated in specific urban areas of Peru, such as Metropolitan Lima, Arequipa, Ica, Piura, and Otuzco, which shows a scientific production focused on specific territorial contexts and not necessarily representative of the entire country. This characteristic suggests that the available evidence remains fragmented and localized.

It was also observed that not all studies directly analyzed digital wallets as a payment method. Some works focused on related technologies, such as digital banking, crowdlending, or financial innovation in FinTech startups, which broadened the understanding of the Peruvian digital ecosystem, although with an indirect relationship to the central objective of the review. Among the wallets specifically mentioned, Yape and Plin were the most recurrent, followed by Tunki, Lukita, and Agora Pay, reflecting their greater presence in recent literature. Finally, the table showed that the units of analysis were diverse, ranging from individual users to microentrepreneurs, SMEs, retail businesses, and FinTech startups, confirming that the phenomenon has been studied from complementary but still dispersed perspectives.

Table 4 | Main findings on entrepreneurship and digital wallets in Peru

|

No. |

Citation |

Main findings |

Evidence on entrepreneurship with digital wallets in Peru |

Limitations reported in the study |

|

1 |

Vilcanqui Velazquez et al. (2022) |

Peru showed favorable conditions for expanding financial inclusion through mobile wallets. Mobile infrastructure, informality, and the need for financial access make FinTech a path for expanding services. |

Indirect evidence. The study argued that mobile wallets and similar services can benefit microenterprises and entrepreneurs by facilitating payments, remittances, and access to financial services. |

It did not empirically assess Peruvian entrepreneurs or measure sales, income, or specific business adoption of digital wallets. |

|

2 |

Vera-Acevedo & Iparraguirre-Piedra (2025) |

Perceived quality and user experience positively influenced consumer trust. Trust, in turn, positively affected electronic word of mouth. Perceived risk did not have a significant moderating effect. |

Indirect evidence. The study suggested that greater trust in digital wallets may encourage continued use in commercial environments, indirectly benefiting businesses that accept payments through these applications. |

The study was limited to users aged 18 to 40 in Metropolitan Lima. It did not directly study MSMEs, ventures, or business indicators. |

|

3 |

Juarez-Alvarez et al. (2025) |

Eighty-eight percent of microentrepreneurs considered digital wallets easy to use; 81% showed a positive attitude; and 80% stated that these tools increased their customer reach and sales. A high correlation was also found between frequency of use and sales growth (rho = 0.820). |

Direct and strong evidence. The study showed that digital-wallet use had a positive impact on the commercial performance of Peruvian microentrepreneurs, especially in sales and customer acquisition. |

The sample was limited to one shopping center in Arequipa and was selected by convenience. Other regions and economic sectors beyond commerce were not included. |

|

4 |

Gomez et al. (2022) |

MSMEs in Piura showed willingness to demand digital financing through crowdlending, valuing lower financial costs and greater flexibility. |

Indirect evidence. Although it did not address digital payment wallets, it showed the openness of Peruvian entrepreneurship to FinTech solutions and financial digitalization. |

The study focused on crowdlending rather than digital wallets; therefore, its relationship with mobile payments was tangential. |

|

5 |

Vargas Garcia (2021) |

A very high positive correlation was found between digital-banking penetration and financial inclusion in Peru (r = 0.982). The study concluded that banking digitalization favors access to financial services. |

Indirect evidence. The study showed that a more digitalized financial environment could facilitate conditions for the development of ventures and small businesses. |

The analysis was aggregated at the national level and did not distinguish entrepreneurs, MSMEs, or specific digital wallets. |

|

6 |

Salazar-Rebaza et al. (2024) |

Before training, 96% of merchants feared using electronic wallets because of cybercrime concerns. After the training and follow-up program, 98% recognized the importance of their use and improved their commercial transactions. |

Direct evidence. The study demonstrated that training in the use of electronic wallets improved transactions, energized operations, facilitated payments to suppliers and services, and strengthened SME competitiveness. |

The study was conducted only in Otuzco and with a relatively small sample. Specific digital-wallet brands were not differentiated. |

|

7 |

Guardamino & Tostes (2021) |

TasaTop was found to be the FinTech startup best prepared to innovate services. The strongest process was technological planning and the weakest was customer training. |

Indirect evidence. The study contributed knowledge on FinTech entrepreneurship in Peru and its innovation capacity, although it did not address digital-wallet use by traditional entrepreneurs. |

It did not analyze digital wallets, sales, or user microenterprises; it focused on the internal technology management of FinTech startups. |

|

8 |

Mendoza Rejas et al. (2023) |

A total of 64.9% of retail entrepreneurs had a positive attitude toward mobile wallets; 57% reported satisfaction; 56.9% considered them efficient and effective; and around 50% still expressed doubts about security, privacy, and regulatory knowledge. |

Direct evidence. The study showed that mobile wallets became an alternative payment method for small businesses in Ica during the pandemic, supporting business continuity and digital adaptation. |

The data came from perceptions of formal retail entrepreneurs in Ica. Actual sales or longitudinal economic results were not measured. |

Table 4 showed that the reviewed studies provided different levels of approximation to the link between entrepreneurship and digital wallets in Peru. Vilcanqui Velazquez et al. (2022) and Vargas Garcia (2021) offered contextual evidence on financial inclusion and digitalization, showing favorable conditions for the expansion of these services. Vera-Acevedo and Iparraguirre-Piedra (2025) highlighted the role of consumer trust as a factor that can encourage the continued use of digital wallets in commercial environments. Juarez-Alvarez et al. (2025) presented one of the most direct pieces of evidence by identifying a positive impact on sales and customer acquisition among microentrepreneurs. Gomez et al. (2022) and Guardamino and Tostes (2021) broadened the discussion from the FinTech ecosystem and financial innovation, albeit indirectly. Salazar-Rebaza et al. (2024) showed that training improves adoption and transactional performance among SMEs. Finally, Mendoza Rejas et al. (2023) confirmed that mobile wallets supported business continuity among retail businesses, although concerns about security and regulation persisted.

DISCUSSION

General synthesis of the findings

The results of this systematic review show that the available scientific evidence on entrepreneurship and digital wallets in Peru is still limited, recent, and methodologically diverse, although it presents consistent trends. In general terms, the reviewed studies suggest that digital wallets are tools with the potential to strengthen the commercial activities of microentrepreneurs, retail businesses, and small firms, especially in contexts where transaction speed, reduced cash use, and closeness to customers are strategic factors.

In relation to the objective of this review, which was to identify sources that provide evidence of entrepreneurship involving digital wallets in Peru, it was observed that not all included studies addressed this relationship directly. However, together they made it possible to build a broad view of the phenomenon, integrating evidence on commercial use, financial inclusion, consumer trust, the FinTech ecosystem, and technological innovation.

Direct evidence on entrepreneurship and digital wallets

The studies by Juarez-Alvarez et al. (2025), Salazar-Rebaza et al. (2024), and Mendoza Rejas et al. (2023) offered the most direct evidence on the relationship between digital wallets and entrepreneurship in Peru. These studies agreed that the use of digital wallets favored specific dimensions of business performance, such as increased sales, expanded customer reach, faster collections and payments, and improved business operations.

Specifically, Juarez-Alvarez et al. (2025) reported that 80% of the surveyed microentrepreneurs stated that the use of digital wallets increased their customer reach and sales. They also found a high correlation between frequency of use and sales growth, which constitutes relevant empirical evidence of the positive impact of these tools on commercial entrepreneurship. Salazar-Rebaza et al. (2024), in turn, demonstrated that the incorporation of electronic wallets, combined with training and follow-up, strengthened SMEs' commercial transactions, facilitated payments to suppliers, and improved competitiveness. Finally, Mendoza Rejas et al. (2023) found that mobile wallets became an important alternative payment method for retail businesses during the pandemic, enabling commercial continuity in a context of health restrictions.

These findings support the assertion that empirical evidence exists regarding the contribution of digital wallets to Peruvian entrepreneurship, although this evidence remains concentrated in local studies and specific sectoral contexts.

Indirect evidence and contextual factors

In addition to direct evidence, the review identified a group of studies that provided important contextual elements for understanding the phenomenon. This group included the works of Vilcanqui Velazquez et al. (2022), Vera-Acevedo and Iparraguirre-Piedra (2025), Gomez et al. (2022), Vargas Garcia (2021), and Guardamino and Tostes (2021).

These studies did not directly measure the impact of digital wallets on specific business indicators, but they offered valuable information about the environment in which these technologies are embedded. For example, Vilcanqui Velazquez et al. (2022) noted that the Peruvian context presents favorable conditions for the expansion of FinTech solutions oriented toward financial inclusion, especially due to factors such as mobile penetration, informality, and the need for access to financial services. Similarly, Vargas Garcia (2021) found a very high correlation between digital banking and financial inclusion in the country, suggesting that digitalization of the financial system creates a more favorable environment for the development of economic and commercial activities.

Likewise, Vera-Acevedo and Iparraguirre-Piedra (2025) showed that consumer trust is strengthened by perceived quality and user experience, which is essential for continued use of electronic wallets in consumption and commercial environments. In the same vein, Guardamino and Tostes (2021) provided evidence on the technological maturity of Peruvian FinTech startups, showing that innovation and technology management are key factors for strengthening the digital financial ecosystem.

Ease of use, acceptance, and perceived value

One of the most consistent findings of the review was the positive perception of the ease of use of digital wallets. Across different studies, users and entrepreneurs valued these tools as simple, fast, useful, and functional. This pattern was especially visible in the findings of Juarez-Alvarez et al. (2025), who reported that 88% of microentrepreneurs considered digital wallets easy to use. Similarly, Mendoza Rejas et al. (2023) found that most retail entrepreneurs had a favorable attitude toward their use and considered them efficient and effective.

Ease of use and perceived value are fundamental factors for the adoption of technological tools in small businesses, especially in contexts where technical, financial, and human resources are limited. In the case of digital wallets, these characteristics appear to be decisive because they reduce entry barriers and allow entrepreneurs to quickly incorporate new payment methods into their daily operations.

The results of Vera-Acevedo and Iparraguirre-Piedra (2025) also reinforce this interpretation by demonstrating that user experience and perceived quality positively influence consumer trust. This suggests that technological acceptance does not depend solely on the existence of an application, but also on how well it responds to expectations of security, speed, and practicality.

Financial inclusion and transformation of the entrepreneurial ecosystem

The review also made it possible to discuss the role of digital wallets within a broader framework of financial inclusion. Several studies suggested that these technologies not only simplify payments but also broaden access to financial services for people and businesses historically excluded from the traditional banking system.

In this regard, Vilcanqui Velazquez et al. (2022) and Vargas Garcia (2021) agreed that financial digitalization can act as a mechanism for economic integration. This point is especially relevant in the Peruvian case, where business informality and low levels of bank access have represented persistent barriers to the development of micro and small enterprises. By requiring lower entry costs and operating through mobile phones, digital wallets reduce part of these barriers and facilitate basic financial transactions.

Although the study by Gomez et al. (2022) did not focus on digital wallets, it showed that Peruvian MSMEs are willing to adopt FinTech solutions for financing, suggesting a broader openness of Peruvian entrepreneurship to financial digitalization. Thus, digital wallets should be understood not only as payment methods but also as part of a broader digital financial ecosystem that can contribute to strengthening entrepreneurship.

Persistent barriers: trust, security, and preference for cash

Despite the benefits identified, the review also showed that the adoption of digital wallets faces important barriers. The most recurrent barrier was distrust associated with security, privacy, cybercrime, and lack of regulatory knowledge. This barrier appeared clearly in the study by Salazar-Rebaza et al. (2024), where 96% of merchants initially expressed fear of using electronic wallets due to concerns about fraud or cybercrime. Similarly, Mendoza Rejas et al. (2023) found relevant doubts about security and privacy among retail entrepreneurs in Ica.

These barriers are compounded by the persistence of cash use as a dominant cultural practice. Even in studies where the benefits of digital wallets were recognized, a preference for cash continued to appear, due to a sense of control, the visibility of money, or transactional habit. This aspect is important because it shows that the transition to digital payment methods depends not only on technological availability but also on the transformation of everyday habits, perceptions, and economic practices.

Therefore, the expansion of digital wallets in Peruvian entrepreneurship requires attention not only to technological access but also to trust building. This implies strengthening platform security, improving institutional communication, expanding digital education, and providing user support.

Importance of training and support

Training emerged as a decisive factor in the successful adoption of digital wallets. The study by Salazar-Rebaza et al. (2024) was particularly illustrative in this regard, as it showed that after a process of training and monitoring, 98% of merchants recognized the importance of using electronic wallets in their regular operations. This demonstrated that initial rejection did not necessarily imply structural opposition to the technology, but rather a lack of information, familiarity, or perceived security.

This result has relevant implications for entrepreneurship-promotion and financial-inclusion programs. Digital wallets can be highly functional, but their effective incorporation requires training processes that enable entrepreneurs to understand their benefits, risks, and uses. In other words, digital and financial literacy appears as a necessary condition for transforming an available tool into one that is truly leveraged.

Methodological considerations of the reviewed evidence

From a methodological perspective, the review showed that most studies used a quantitative approach and relied on surveys, descriptive and correlational analyses, or technology-acceptance models. This made it possible to identify patterns, relationships, and general trends, but limited the in-depth understanding of the cultural, organizational, and social processes involved in digital-wallet adoption.

Only one study used a qualitative approach and another a mixed approach, revealing a limited presence of research aimed at exploring in depth entrepreneurs' experiences and contextual adoption factors. Moreover, several studies used localized samples concentrated in cities such as Lima, Arequipa, Ica, Piura, and Otuzco. This means that, although the evidence found is valuable, the findings should be interpreted with caution, as they do not necessarily represent the national reality as a whole.

Another important limitation is that several studies were based on participants' perceptions rather than objective indicators of business performance. Therefore, although positive associations were identified between digital wallets and sales or commercial transactions, the empirical basis still needs to be strengthened through longitudinal, comparative studies using verifiable economic data.

Practical and academic implications

From a practical perspective, the results suggest that digital wallets can be considered a strategic tool for strengthening Peruvian entrepreneurship, especially among micro and small economic units. Their use can contribute to improving customer relationships, speeding up collections and payments, expanding commercial coverage, and facilitating the integration of small businesses into more modern exchange dynamics.

For policymakers, these findings indicate the need to promote actions aimed at strengthening digital trust, training in the use of financial technology tools, and expanding connectivity in regions where adoption remains limited. For financial institutions and digital-wallet developers, the results show the importance of designing simple, secure solutions adapted to the needs of small businesses.

From an academic perspective, the review showed that the field is still under construction. There have been important advances, but further research is still needed on entrepreneurship, digital wallets, and business performance in the Peruvian context.

Identified research gaps

Finally, the discussion identified several gaps in the literature. First, studies are needed that directly analyze the impact of digital wallets on variables such as profitability, formalization, business sustainability, and business growth. Second, research comparing the effects of specific wallets, especially Yape and Plin, which were the most frequently mentioned platforms in the reviewed studies, is required. Third, it is necessary to broaden the geographic and sectoral coverage of research by incorporating rural regions, non-commercial sectors, and ventures led by different entrepreneur profiles.

There is also a need for longitudinal studies to determine whether the observed benefits in sales and transactions are sustained over time. It would also be relevant to integrate qualitative or mixed methodologies to better understand how entrepreneurs perceive, negotiate, and adapt these technologies in their everyday practice.

Final conclusions

In summary, the review concludes that digital wallets represent an innovation with a favorable impact on Peruvian entrepreneurship, especially in microventures, retail businesses, and small enterprises. The most direct evidence showed benefits in sales, commercial reach, and operational efficiency, while indirect evidence reinforced the idea that these tools are part of a broader process of financial inclusion and digital transformation. However, the persistence of barriers associated with security, trust, and preference for cash shows that their consolidation still faces challenges. Therefore, strengthening this field requires both new research and practical interventions aimed at expanding the use and value of digital wallets in Peru's entrepreneurial ecosystem.

Authors' statement: The authors approve the final version of the article.

Conflict-of-interest statement: The authors declare no conflicts of interest.

Authors' contributions:

- Conceptualization: Victor Hugo Fernandez-Bedoya, Johanna de Jesus Stephanie Gago-Chavez

- Data curation: Victor Hugo Fernandez-Bedoya, Monica Elisa Meneses-La-Riva

- Formal analysis: Victor Hugo Fernandez-Bedoya, Josefina Amanda Suyo-Vega

- Investigation: Victor Hugo Fernandez-Bedoya, Josefina Amanda Suyo-Vega

- Methodology: Victor Hugo Fernandez-Bedoya, Monica Elisa Meneses-La-Riva

- Writing - original draft: Victor Hugo Fernandez-Bedoya, Johanna de Jesus Stephanie Gago-Chavez, Monica Elisa Meneses-La-Riva, Josefina Amanda Suyo-Vega

- Writing - review and editing: Victor Hugo Fernandez-Bedoya, Johanna de Jesus Stephanie Gago-Chavez, Monica Elisa Meneses-La-Riva, Josefina Amanda Suyo-Vega

Funding: This work was self-funded.

REFERENCES

Antúnez, A. M. C., Morales, C. E. B., & Araujo, D. R. S. (2019). La sostenibilidad global en una empresa de transporte urbano de viajeros en autobús: Estudio de caso. In Memorias del III Congreso internacional en administración de negocios internacionales (CIANI): Retos y oportunidades del desarrollo sostenible en los negocios internacionales (pp. 28-42). Universidad Pontificia Bolivariana.

Arrieta, L. E., & Morales, C. E. B. (2024). Necesidades sociales y dimensiones del capital social: análisis de beneficiarios de Familias en Acción. Telos: Revista de Estudios Interdisciplinarios en Ciencias Sociales, 26(2), 388-407.

Arner, D. W., Buckley, R. P., Zetzsche, D. A., & Veidt, R. (2020). Sustainability, FinTech and financial inclusion. European Business Organization Law Review, 21(1), 7-35. https://doi.org/10.1007/s40804-020-00183-y

Banco Central de Reserva del Perú. (2021). Reporte de estabilidad financiera: Mayo 2021. BCRP. https://www.bcrp.gob.pe/docs/Publicaciones/Reporte-Estabilidad-Financiera/2021/mayo/ref-mayo-2021.pdf

Banco Central de Reserva del Perú. (2023). Reporte de estabilidad financiera: Mayo 2023. BCRP. https://www.bcrp.gob.pe/docs/Publicaciones/Reporte-Estabilidad-Financiera/2023/mayo/ref-mayo-2023.pdf

Barrera, M. B., & Morales, C. E. B. (2025). Análisis de la percepción de la cultura tributaria en Colombia durante el periodo pospandemia. Dictamen Libre, (36), 2.

Borja-Barrera, M., & Barragán-Morales, C. (2025). Perception analysis of tax culture in Colombia during the post-pandemic period. Dictamen Libre, (36).

Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The Global Findex Database 2017: Measuring financial inclusion and the fintech revolution. World Bank Publications. https://doi.org/10.1596/978-1-4648-1259-0

Espitia-Arrieta, L., Tatiana Prestan-Gómez, S., & Barragán-Morales, C. (2022). Programas de transferencias monetarias condicionadas: una comparación en América Latina frente a Familias en Acción. Dictamen Libre, (31).

Fábregas-Rodado, C., Miranda-Passo, J., Londoño-Carpio, M., & Vargas-Peñaranda, M. (2023). Capacidades organizacionales requeridas en las industrias creativas del sector “hacedores del carnaval de Barranquilla”. Revista Económica, 11(2), 9–17. https://doi.org/10.54753/rve.v11i2.1681

Gabor, D., & Brooks, S. (2017). The digital revolution in financial inclusion: International development in the fintech era. New Political Economy, 22(4), 423-436. https://doi.org/10.1080/13563467.2017.1259298

Global Entrepreneurship Monitor. (2022). GEM 2021/2022 Global Report: Opportunity amid disruption. GEM. https://www.gemconsortium.org/report/gem-20212022-global-report-opportunity-amid-disruption

Gómez, G., Navarro-Barranzuela, J. A., & Marchena-Ojeda, L. M. (2022). El crowdlending como alternativa de financiamiento para las mipymes del Perú. Retos. Revista de Ciencias de la Administración y Economía, 12(23), 161–177. https://doi.org/10.17163/ret.n23.2022.10

Guardamino, H., & Tostes, M. (2021). Análisis cualitativo de la gestión tecnológica para la innovación de servicios financieros: Estudio de casos múltiples de startups FinTech en Lima Metropolitana. New Trends in Qualitative Research, 9, 218–227. https://doi.org/10.36367/ntqr.9.2021.218-227

Hernández, J. ., & Castillo, A. (2021). La creación de valor: un enfoque actual de la gestión empresarial. Ad-Gnosis, 10(10), 151-168. https://doi.org/10.21803/adgnosis.10.10.476

Herrera, D., & Vadillo, S. (2022). Billeteras móviles en el Perú: Un ecosistema en consolidación. Banco Interamericano de Desarrollo. https://publications.iadb.org/es/billeteras-moviles-en-el-peru

Juarez-Alvarez, C. R., Merino-Lazo-De-La-Vega, V. P., Villanueva-Paredes, G. X., & Esquicha-Tejada, J. D. (2025). Adoption of digital wallets and their impact on the sales of Peruvian micro-entrepreneurs. Polish Journal of Management Studies, 31(1), 158–177. https://doi.org/10.17512/pjms.2025.31.1.09

Mendoza Rejas, J. N., Huamán, R. de la C., Canchari Vásquez, U., & Motta Dueñas, J. A. (2023). Billeteras móviles, medio de pago alternativo para minoristas en pandemia. Investigación Negocios & Revista Científica, 16(28), 14–21. https://doi.org/10.38147/invneg.v16i28.162

Morales, C. E. B., De Moya, F. E. M., Vélez, N. S., & Vargas, E. C. (2023). Innovación social: Una aproximación desde su relación con la responsabilidad social empresarial en tiempos del COVID 19. In Investigación y Desarrollo (pp. 137-150). Fondo Editorial CIIDIES.

Morales, C. E. B., Guarín-García, A. F., Chang-Muñoz, E. A., Villanueva-Vásquez, A., Gálvez, J. F. E., Delgado, N. A. G., & Bracho, O. C. (2025). Fuzzy-Set Qualitative Comparative Analysis to Corporate Social Responsibility Components: A Case Study from Media Print Companies in Atlántico Department of Colombia. Procedia Computer Science, 257, 1148-1153.

Morales, C. E. B., Mendoza, A. P., Barrera, M. B., & Osorio, F. M. (2024). Transformational leadership and decision-making in organizations of the Colombian Caribbean. Dictamen Libre, (34), 167-178.

Mudarra-Fernández, A. B., Barragán-Morales, C. E., & González-Beleño, C. (2023). La eficiencia de las empresas con marca en los hoteles de las Ciudades Patrimonio de la Humanidad consolidadas de España. Revista Ibérica de Sistemas e Tecnologias de Informação, (E60), 624-636.

Nambisan, S. (2017). Digital entrepreneurship: Toward a digital technology perspective of entrepreneurship. Entrepreneurship Theory and Practice, 41(6), 1029-1055. https://doi.org/10.1111/etap.12254

Organismo Supervisor de Inversión Privada en Telecomunicaciones. (2023). Reporte estadístico: Indicadores del servicio móvil. OSIPTEL. https://www.osiptel.gob.pe/portal-del-usuario/reportes-estadisticos/

Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., Chou, R., Glanville, J., Grimshaw, J. M., Hróbjartsson, A., Lalu, M. M., Li, T., Loder, E. W., Mayo-Wilson, E., McDonald, S., ... Moher, D. (2021). The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ, 372, n71. https://doi.org/10.1136/bmj.n71

Salazar-Rebaza, C., Zurita-Guerrero, G., & Ibañez-Luján, W. (2024). Use of e-wallets and their impact on SME business transactions. In Proceedings of the 19th European Conference on Innovation and Entrepreneurship (pp. 694–702). https://papers.academic-conferences.org/index.php/ecie/article/view/2596

Sandoval Reyes, R. ., Roncallo Pichón, A. J., Barrientos Pérez, E. ., & Landazury Villalba, L. F. (2020). Incremento en la base gravable del impuesto predial en el distrito de Barranquilla en 2018. Ad-Gnosis, 9(9), 59-68. https://doi.org/10.21803/adgnosis.9.9.437

Serida, J., Guerrero, C., Alzamora, J., Borda, A., & Morales, O. (2020). Global Entrepreneurship Monitor: Perú 2019-2020. ESAN Ediciones. https://www.esan.edu.pe/publicaciones/libros/2020/global-entrepreneurship-monitor-peru-2019-2020/

Turizo, J. M., Bracho, O. C. C., & Morales, C. B. (2026). General and differential mechanisms of citizen participation: Prior consultation and victims’ participation boards. Pensamiento Americano, 19(39).

Vargas Garcia, A. H. (2021). Digital banking: Technological innovation in financial inclusion in Peru. Industrial Data, 24(2), 99–120. https://doi.org/10.15381/idata.v24i2.20351

Vera-Acevedo, A. V., & Iparraguirre-Piedra, M. F. (2025). The influence of consumer trust on the drivers of electronic wallet transactions. Intangible Capital, 21(3), 427–449. https://doi.org/10.3926/ic.3195

Vilcanqui Velazquez, P., Bobek, V., Korez Vide, R., & Horvat, T. (2022). Lessons from remarkable FinTech companies for the financial inclusion in Peru. Journal of Risk and Financial Management, 15(2), Article 62. https://doi.org/10.3390/jrfm15020062